Why There Won’t Be a Flood of Foreclosures Coming to the Housing Market

Courtesy of Keeping Current Matters.

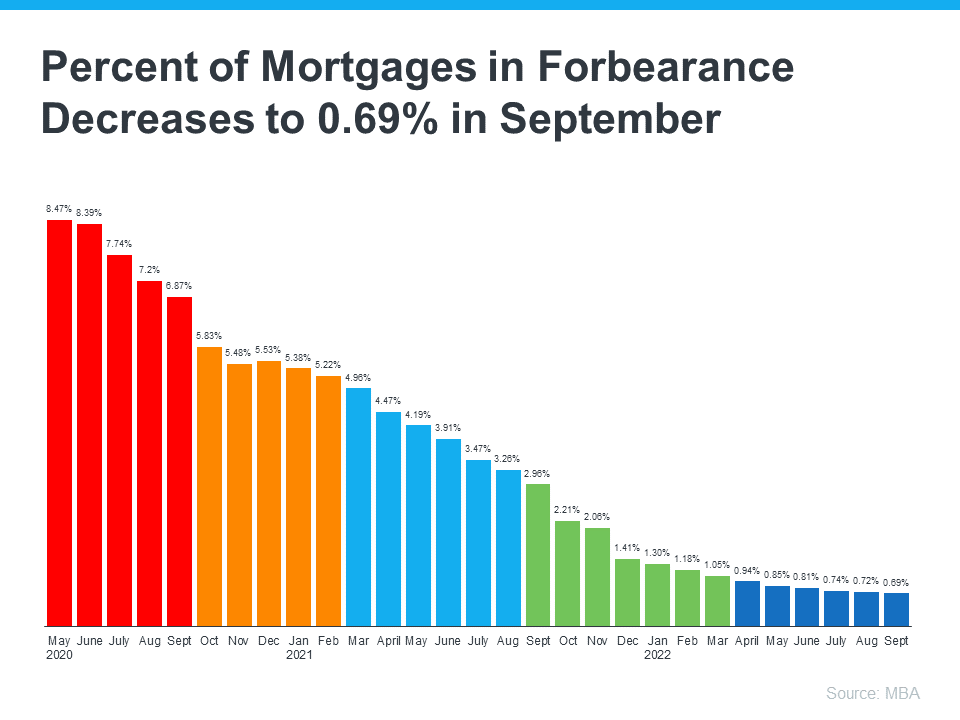

With the rapid shift that’s happened in the housing market this year, some people are raising concerns that we’re destined for a repeat of the crash we saw in 2008. But in truth, there are many key differences between what’s happening today and the bubble in the early [...]